Independent Financial Research & Analysis

Daily briefings, 7,300+ real-time charts, and macro insights from Dr. Ed Yardeni and his research team.

Research

Latest Research

Recent insights from our research team

CONSUMER DISCRETIONARY: Another Concentrated Sector

We recommend a market-weight position in the S&P 500 Consumer Discretionary sector. At first glance, the sector looks strong. Its stock price index is near a record high, forward earnings is rising, and the forward P/E has held in the mid-20s (chart). The surface-level fundamentals are attractive. Look closer, and the strength narrows. Consumer Discretionary is up just 2.3% ytd, ninth among the 11 S&P 500 sectors. Only the sector’s retail industries are positive so far this year. The rest of its industries are down ytd by various amounts running from Automobile Manufacturers, down 4.4%, to Other Specialty Retail, down 25.7% (chart). A handful of names has carried the index’s performance while most of the sector trades lower. Consider the following: (1) Concentration. The sector accounts for just 9.8% of the S&P 500's market capitalization and 7.6% of the index's forward earnings (chart). Amazon and Tesla together account for 62.0% of the sector's market capitalization and 39.9% of its forward earnings (chart). That share has surged in recent weeks. Any call on the sector is mostly a call on these two. (2) Weak breadth. The S&P 500 Consumer Discretionary stock price index is near a record high, while its S&P 400 MidCap and S&P 600 SmallCap counterparts remain well below their 2021 peaks (chart). The smaller discretionary names, closer to the everyday consumer, are lagging the market. This is the K-shaped consumer showing up in the tape, with higher-end spending feeding the LargeCaps while the rest lag. (3) Earnings and revenues growth. Sector earnings growth is set to almost double to 14.6% in 2026, up from 7.7% in 2025 (chart). Revenue growth is far more subdued, ticking up to just 7.5% in 2026 from 5.7% in 2025. (4) Profit margin. At 10.0%, the sector's forward profit margin is the third-lowest of the 11 sectors’ margins, ahead of only Health Care’s and Consumer Staples’ (chart). Retail and autos are inherently low-margin businesses. The margin has climbed to a record over the past decade but off a low base. (5) Valuation. The sector's forward P/E is 26.7, well above the S&P 500's 21.1 (chart). That premium of more than five points partly reflects Tesla's 194.8 multiple, which lifts the sector reading, much as its market cap distorts the sector weight. Strip out that distortion, and the rest of the sector is cheaper than the headline implies. The multiple has been re-rated higher since 2020 and sits near the middle of that range today, neither cheap nor at a peak. (6) Risk appetite. The ratio of the Consumer Discretionary to the Consumer Staples stock price index is 2.07, near a record high (chart). Investors still favor the cyclical consumer over the defensive one. A strong stock price index resting on two stocks, with thin breadth, and a full multiple, is a sector to hold, not to chase. We stay market-weight. It could briefly outperform if ol prices fall in response to the end of the war in the Middle East.

US MARKET CALL: FOMO vs FEMO (Fabulous Earnings Momentum)

The stock market has had an exuberant stretch since the S&P 500 bottomed on March 30. The index is up 17.8% since then through Friday, after hitting a record high on May 14. The DJIA rose to a record high this past Friday. The bears say the exuberance is irrational, driven by lots of excitement about AI. We say it is rational, based on our Buzz Lightyear Theory (BLT) of "To Infinity and Beyond!" According to our BLT, there’s a fourth factor or production, not just the historically recognized three. In addition to land, labor, and capital, which are relatively scarce, there’s now data, the supply of which is unlimited. The Digital Revolution, which began in the 1960s, is all about processing as much information as possible, as quickly as possible and as cheaply as possible. Today's AI technologies can certainly do all that much better than IBM mainframes back in the mid-1960s. Instead of focusing on rational versus irrational exuberance, let's compare FOMO to FEMO. The former stands for “Fear Of Missing Out.” Investors pile into stocks, bidding up their price-to-earnings multiples. FEMO is “Fabulous Earnings Momentum.” Analysts raise their earnings estimates because hard data and company guidance give them reason to do so. We would rather see FEMO than FOMO every time. This year has been all about FEMO. Through Friday, the S&P 500 is up 9.2% ytd, forward earnings is up 14.4%, and the forward P/E is down 4.6% (chart). The entire rally has been driven by forward earnings. The multiple has contracted. FOMO inflates the P/E. This market did the opposite. That is why we are not in the bubble camp. FOMO is based on hope and hype. FEMO is based on fundamentals. At 21.1 times forward earnings, the S&P 500 is not irrationally valued unless a recession is coming in the foreseeable future. We don't see one. Now consider the following: (1) Record forward earnings. The S&P 500's forward EPS rose further to a record $358.82 last week. The 2026 and 2027 consensus earnings estimates are both at new highs of $337.11 and $390.86, respectively (chart). Analysts keep raising their estimates as the AI compute buildout struggles to keep pace with the exploding demand for processing ever more data. Forward earnings is a leading indicator of the actual quarterly earnings of the S&P 500 (chart). We have rarely seen forward earnings rise so quickly at this stage of an earnings cycle. That's FEMO. (2) Record profit margins. Profit margins have been on fire since mid-2023, approximately seven months after ChatGPT was released. The forward profit margin reached a record 15.5% last week, and the current 2027 consensus margin is 16.1%, up from 14.8% currently this year (chart). This is consistent with the productivity gains at the heart of our Roaring 2020s narrative. (3) Broadening earnings breadth. Across the S&P 500, 85.6% of companies report rising forward earnings, and 89.0% report rising forward revenues, both on a y/y basis (chart). That's more FEMO. (4) Mag-7 vs Impressive 493. FEMO has been led by the Mag-7 since ChatGPT was released in late 2022. Their combined forward earnings has increased sharply since mid-2023 (chart). There is one caveat: A few of these companies booked mark-to-market gains on their AI investments in Q1-2026, which boosted reported earnings. Strip those out, and the underlying growth rate remains solid. Meanwhile, the forward earnings of the Impressive 493 has also been rising faster in recent months, to record-high territory. (5) FEMO and LTEG. Fabulous Earnings Momentum has been driven by the rising consensus of long-term earnings growth (LTEG) expectations of industry analysts. Information Technology alone is the biggest contributor to the S&P 500's LTEG. It is the only sector above the S&P 500's LTEG, at 34.9% versus the index's 21.9% (chart). That 34.9% is a record high, above its dot-com peak (chart). Information Technology's growth expectations may be bordering on irrational, and we flag it. But this is analysts raising LTEG, not investors bidding up stock prices. Optimistic earnings forecasts get revised. They do not crash the market the way that a stretched valuation multiple can. (6) Valuation and FOMO. The multiple is where FOMO resides, but it is nowhere to be found. The S&P 500 trades at 21.1 times forward earnings per share, and the Information Technology sector at 24.4 (chart). In 2000, the multiple ran up while earnings lagged behind. This year, it is the reverse: Earnings is doing the running, and the multiple has backtracked. That is the better setup. That is FEMO, not FOMO. (7) Case study. Semiconductors make the case. The industry's share of Information Technology's forward earnings has risen to 46.9%, only slightly above its 45.1% share of the sector's market cap (chart). The market is signaling that semiconductor makers are growth companies, not the cyclicals they once were. That conviction would normally inflate their stocks’ P/E multiples. It hasn't. The rally in the semis has been led by E, not P/E. That is FEMO, not FOMO.

ECONOMIC WEEK AHEAD: May 25-29

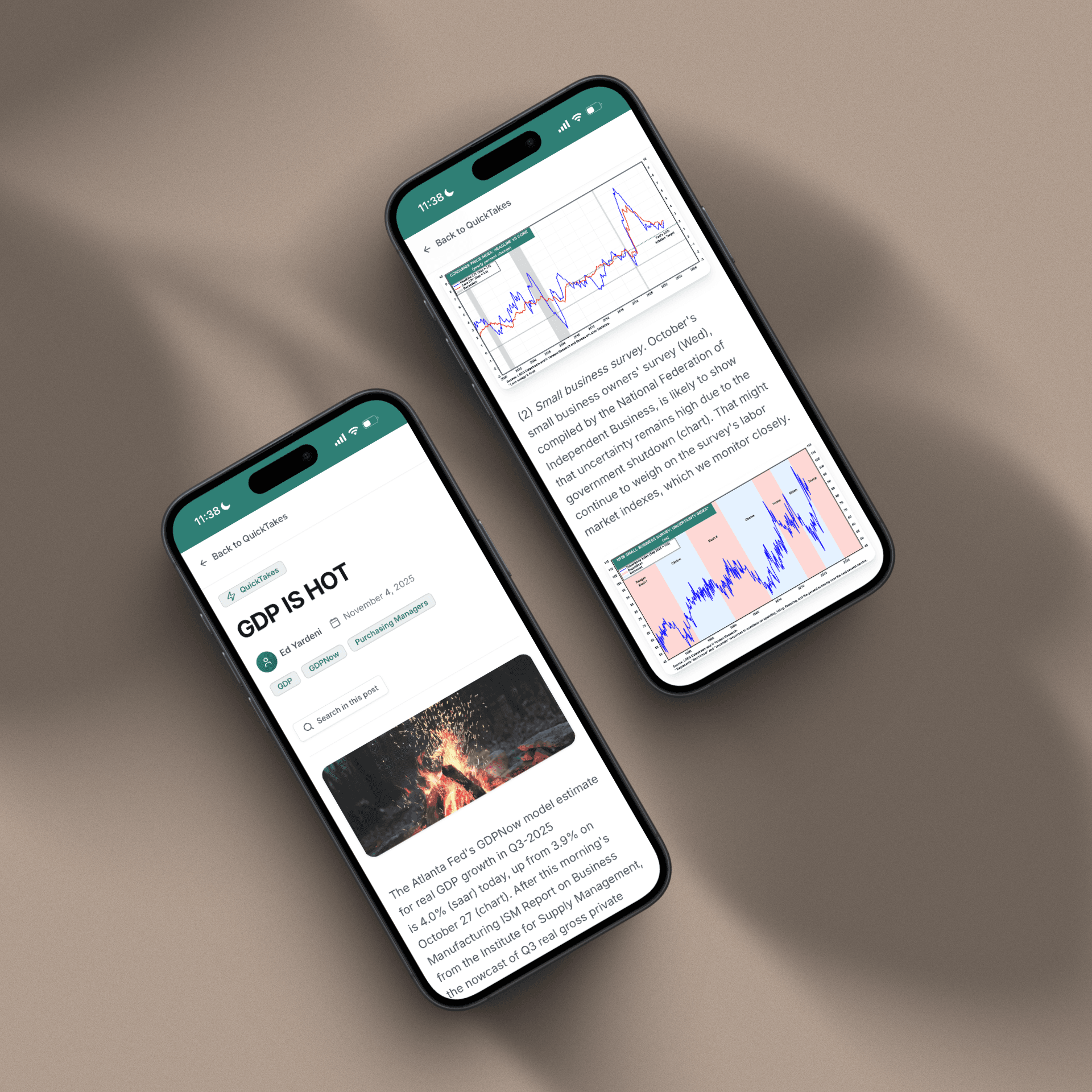

The US financial markets are closed on Monday for Memorial Day, and the holiday-shortened week is light on economic data releases. On Thursday, the second estimate of Q1-2026 GDP will be reported alongside April's core PCED, the Fed's preferred inflation gauge. Eight Fed officials speak over the week. With little fresh data to help investors gauge whether the FOMC is turning more hawkish, they’ll be parsing the speakers’ commentary for signs. The markets now reflect a 62.5% chance of a rate hike this year, arriving in December, up from 50.0% a week ago. We think one could come as early as July. The wild card is whether President Donald Trump's latest "likely negotiated" peace deal is the real deal. On Saturday, he said that it would reopen the Strait of Hormuz. The deal under discussion includes a memorandum of understanding as a first phase, Iran’s foreign ministry said Saturday, with broader talks to follow within 30 to 60 days. The two sides remain far apart on key issues. Globally, bond yields backed off this week’s highs but stayed elevated. The 10-year US Treasury yield eased to 4.56% from a 4.69% peak, and the UK 10-year gilt slipped to 4.90% from 5.19% (chart). Here are the key economic releases most likely to shape investors’ thinking this week: (1) GDP. Thursday's second estimate of Q1-2026 GDP should hold near the 2.0% advance reading. The Atlanta Fed's GDPNow model already has Q2 tracking 4.3%, led by a surge in business equipment spending (chart). (2) Core PCED. April's core PCED, the Fed's preferred inflation gauge, arrives Thursday. It ran at 3.2% y/y in March, up from 3.0% in February, with headline inflation at 3.5% (chart). Given that the latest CPI and PPI both ran hot, the risk is another upside surprise that further strengthens the case for a Fed rate hike. (3) Consumer confidence. May's Consumer Confidence Index survey (Tue) should tick higher from April's 92.8 (chart). We will focus on the labor market indicators, which are likely to show some improvement. (4) Unemployment. Initial jobless claims (Thu) came in at 209,000, with the four-week moving average at 202,500 (chart). Continuing claims were 1,782,000, with the four-week moving average at 1,778,000. The labor market continues to improve. (5) Regional business surveys. The week's regional Fed business surveys include Dallas (Tue) and Richmond (Wed). Both the ISM national M-PMI and the regional average of the five Fed surveys have turned higher in recent months (chart). The recovery in manufacturing is broadening. The regional prices-paid average has climbed back to 54.9, and PPI final demand is already running at 6.0% y/y (chart).

Archive

Our Research Library

19 years of daily research, charts, and analysis

Topics

QuickTakes Topics

Timely commentary covering the most important market themes

Charts

Find Any Chart in Seconds

Search across 7,349+ real-time charts with instant visual previews

PHILIP MORRIS INTERNATIONAL: FORWARD LTEG, STRG & STEG

TARGET: FORWARD PROFIT MARGIN

S&P 500 TRANSACTION & PAYMENT PROCESSING SERVICES: FORWARD STEG & LTEG

BNY MELLON: FORWARD LTEG, STRG & STEG

Sample charts from our collection of 7,349+ visualizations

Tools

Research Tools

Interactive dashboards for tracking economic conditions and market trends

Beige Book Monitor

Fed economic conditions across 12 districts with traffic-light signals.

FOMC Policy Meter

Dovish-to-hawkish policy stance tracker across FOMC meetings.

FOMC Minutes Monitor

Hawk/dove signal extraction across 10 economic themes.

FOMC SEP Monitor

Fed projections and dot plot distributions across meetings.

Private Credit Monitor

Auto-updating chronology of the private credit liquidity crisis.

Release Calendar

Major publications from the Fed, ECB, IMF, and 12 global institutions.

Try Yardeni Research free for four weeks.

Full access to everything we publish. No credit card, no obligation.