Independent Financial Research & Analysis

Daily briefings, 7,500+ real-time charts, and macro insights from Dr. Ed Yardeni and his research team.

Research

Latest Research

Recent insights from our research team

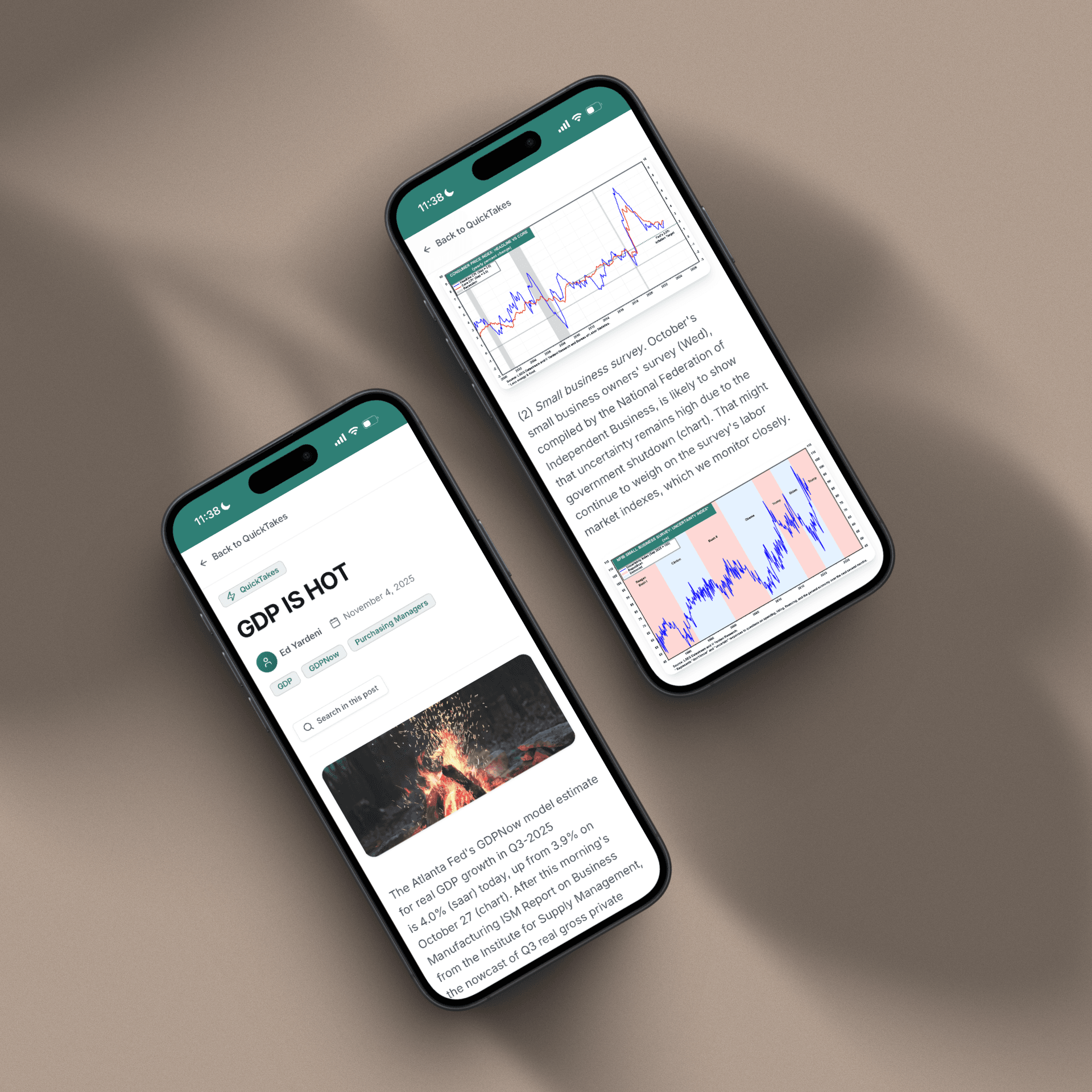

People Close To Warsh Are Talking About Him

I. The Fed Today's Financial Times ran an exclusive story about Fed Chair Kevin Warsh. It is based on insights provided by unidentified people close to him. They say that he admits that he has made some mistakes, "including failing to reinforce his key messages on price stability." In our opinion, he has been unequivocal about his commitment to restore price stability. He just hasn't done anything about it so far. Nor has he provided any information about the Fed's reaction function under his leadership. The FT article suggests he is watching "market-based measures of inflation," which remain low. Furthermore, the article states, "[b]y breaking the feedback loop between the Fed and investors, the new chair has said that he hopes markets will spend less time scrutinising officials’ clues and focus more on economic data." We've been monitoring the 2-year Treasury yield, which is unambiguously calling for rate hikes. Warsh is refusing to provide any forward guidance, but his people are providing some, saying that he is "prepared to raise interest rates at September’s meeting if inflation readings released in coming weeks are hot." We thought that the Q2-2026 core GDP deflators for total GDP and for personal consumption expenditures were hot at 3.8% y/y and 3.3% (chart). Will Warsh provide any more clarity in his Jackson Hole speech on Friday, August 28. We doubt it. II. Macro The September FOMC rate decision will ultimately hinge on the economic data. The latest reports point to a resilient economy, a tight labor market, and persistent inflation pressures. Consider the following: (1) Productivity. Productivity, measured as nonfarm business output per hour worked, rose 2.2% y/y in Q2, in line with its 2.1% long-term average (chart). We expect productivity growth to improve over the rest of the decade as businesses continue investing heavily in AI and other productivity-enhancing technologies. That should boost economic growth and moderate inflation. For now, AI is boosting inflation, as we have previously discussed. (2) Unit labor costs & inflation. Unit labor costs, measured as hourly compensation divided by productivity, rose just 1.4% y/y in Q2 (chart). This suggests that labor market conditions are not a source of inflation. Instead, inflationary pressures are coming from higher energy prices, tariff-related increases in goods prices, and the economy's ongoing AI-driven investment boom. (3) Corporate profitability. Corporate and S&P 500 profit margins remain near record highs, helping to support surprisingly strong earnings growth (chart). Continued productivity gains should provide further support for profits over the remainder of the decade. (4) Initial unemployment claims. Jobless claims rose slightly to 199,000 in the week ending July 31 but remained below 200,000 for a third consecutive week (charts). Even more encouraging, the four-week moving average fell to its lowest level since October 2022, suggesting that the unemployment rate fell in July. Continuing claims also remain subdued. (5) Layoff announcements. The decline in jobless claims is corroborated by layoff announcements. US employers announced just 33,429 job cuts in July, the lowest monthly total in two years (chart). (6) Job growth. Yesterday, ADP reported that private payrolls rose by 44,000 in July. Today Revelio Labs estimated that nonfarm payrolls increased by 79,200. III. Commodities The war isn't over. This afternoon, Reuters reported, "An attack by Yemen's Houthis on southern Saudi Arabia wounded 11 civilians." An Iranian parliamentary committee is reviewing a preliminary bill that would bar US, Israeli and other "hostile" vessels from transiting the Strait of Hormuz, Iran's semi-official Fars news agency reported, citing a lawmaker. Yet, the price of a barrel of Brent crude oil remains below $84 this evening (chart). Meanwhile, the turmoil in the Middle East doesn't seem to be denting global economic growth, according to the copper price, which rose to a record high today (chart). It looks set to move still higher. IV. Stocks The bull-bear ratios we monitor showed increased bullishness this week (chart). They are not high enough to provide clear signals of an imminent pullback.

On SpaceX, Copper & Semiconductors

Have SpaceX investors gotten altitude sickness? As SpaceX, the company, continues to shoot for the moon, SpaceX, the stock, has been spiraling. Jackie examines both Elon Musk’s lofty ambitions for the company and investors’ down-to-earth concerns. … Also: The huge data center buildout is driving up demand for the materials used, from construction machinery to metals. Their pricing reflects the soaring demand. So does the Q2 earnings report of copper producer Freeport-McMoRan. … And in our Disruptive Technology segment: The challenge of making semiconductor chips more efficient.

US Economy Is Fine & The Fed Should Be Turning More Hawkish

I. Macro The economy's two most important engines of economic growth, consumer spending and business investment, are booming. In Q2-2026 real GDP, consumption expenditures increased 3.3% (saar) and nonresidential fixed investments jumped 8.4%. The headline and core GDP deflators, the most comprehensive measures of economy-wide inflation, rose 4.3% y/y and 3.8% (chart). Fed officials should be turning hawkish. Recent Q2 earnings reports were upbeat on consumers. Booking Holdings maintained its full-year outlook and reported solid travel demand despite higher airfares and geopolitical turmoil. Disney also delivered better-than-expected results, with strong performance at its parks and experiences business. Bank of America expects hyperscaler capital expenditures to reach $860 billion this year and approach $1.2 trillion in 2027. The AI buildout has turned into its own stimulus program for the economy. And, of course, the government deficit remains very stimulative. Fed officials appear to be dividing into two camps. One camp views rate hikes as necessary only if inflation fails to fall closer to 2%. Recent comments from Philadelphia Fed President Anna Paulson and Fed Governor Lisa Cook fit broadly into this category. Paulson said she is keeping an "open mind" about whether current monetary policy is sufficiently restrictive. Cook reiterated that she is prepared to act if inflation fails to cool.The other camp wants to hike the federal funds rate sooner rather than later. They include the three dissenters at the FOMC's July meeting. Recent comments from Minneapolis Fed President Neel Kashkari (one of the dissenters) and Kansas City Fed President Jeff Schmid reflect this hawkish view. Kashkari said additional hikes this year are "not impossible" and that "now is the time to start slowly moving up." Schmid argued that "bringing inflation down to the Fed's 2% objective will require tighter policy." He does not view current policy as restrictive. This camp worries that five years of above-target inflation, ongoing supply shocks, and strong economic activity could cause inflation to remain stuck above the Fed's 2.0% inflation target. Financial markets are siding with the more hawkish camp. The 2-year US Treasury note yield remains well above the federal funds rate (chart). The latest economic developments confirm that the upside inflation risks exceed the downside risks to the economy: (1) Employment. On May 7, we wrote that the labor market was likely to improve in the spring and that employment-related stocks might have bottomed. So far, so good. Labor market conditions have improved from the winter months, while the stock prices of ADP, Paychex, and ManpowerGroup have rebounded (chart). Today’s July ADP jobs report showed private employers added 44,000 jobs, down from 95,000 in June (chart). Even so, the three-month average remained at a solid 87,000, a pace that should keep unemployment low (chart). We expect jobs growth to get a lift from the AI investment boom, particularly in manufacturing and construction. We acknowledge that this scenario did not get confirmed by the latest ADP report. (2) Employment Cost Index (ECI). The ECI rose 3.8% (saar) during Q2 and 3.3% y/y, remaining relatively stable (chart). These figures support our view that the labor market remains well balanced. There is no wage-price spiral currently, as there was in 2021 and 2022. ECI wage and salary growth slowed to 3.1% y/y, closer to its pre-pandemic readings (chart). Benefits increased 3.8%. (3) Nonmanufacturing Purchasing Managers. The services PMI edged up to 54.1 in July, as business activity rose to a five-month high and new orders strengthened (chart). The expansion is broad based, with 13 industries reporting growth. The services prices-paid index rose to 70.3 in July, while the manufacturing counterpart remained elevated at 71.1 (chart). These are relatively hot readings. II. Markets The price of gold seems to have found support at $4,000 per ounce in recent days (chart). It rose sharply today and continues to advance this evening. That's giving us more confidence in our year-end target of $5,000. Then again, the latest move higher suggests that gold traders don't agree with our hawkish spin on Fed policy. Today's economic data might have convinced them that the Fed is less likely to raise rates anytime soon. That view was confirmed by the modestly weaker dollar. We are counting on central bank buying to boost the price of gold even if the Fed tightens and the dollar strengthens. After the strong tech-led rally during Monday and Tuesday, the S&P 500 edged down slightly today (chart). The three strongest sectors are among our overweight recommendations. So is Energy, which was weak today on news that Iran and Oman have agreed on precise geographic coordinates for a joint shipping lane through the Strait of Hormuz, enabling 60 days of fee-free commercial transit.

Archive

Our Research Library

19 years of daily research, charts, and analysis

Topics

QuickTakes Topics

Timely commentary covering the most important market themes

Charts

Find Any Chart in Seconds

Search across 7,552+ real-time charts with instant visual previews

BNY MELLON: FORWARD OPERATING EARNINGS PER SHARE

PHILIP MORRIS INTERNATIONAL: FORWARD REVENUES

NIKE: FORWARD REVENUES

NIKE: STOCK PRICE (NKE)

Sample charts from our collection of 7,552+ visualizations

Tools

Research Tools

Interactive dashboards for tracking economic conditions and market trends

Beige Book Monitor

Fed economic conditions across 12 districts with traffic-light signals.

FOMC Policy Meter

Dovish-to-hawkish policy stance tracker across FOMC meetings.

FOMC Minutes Monitor

Hawk/dove signal extraction across 10 economic themes.

FOMC SEP Monitor

Fed projections and dot plot distributions across meetings.

FOMC Statements

Every FOMC policy statement since 1997 — full text, rates, and voting records.

Private Credit Monitor

Auto-updating chronology of the private credit liquidity crisis.

Release Calendar

Major publications from the Fed, ECB, IMF, and 12 global institutions.

Try Yardeni Research free for four weeks.

Full access to everything we publish. No credit card, no obligation.